The Asymmetric Cost of Money: Why the Consumer Yield Rail is Migrating Off-bank

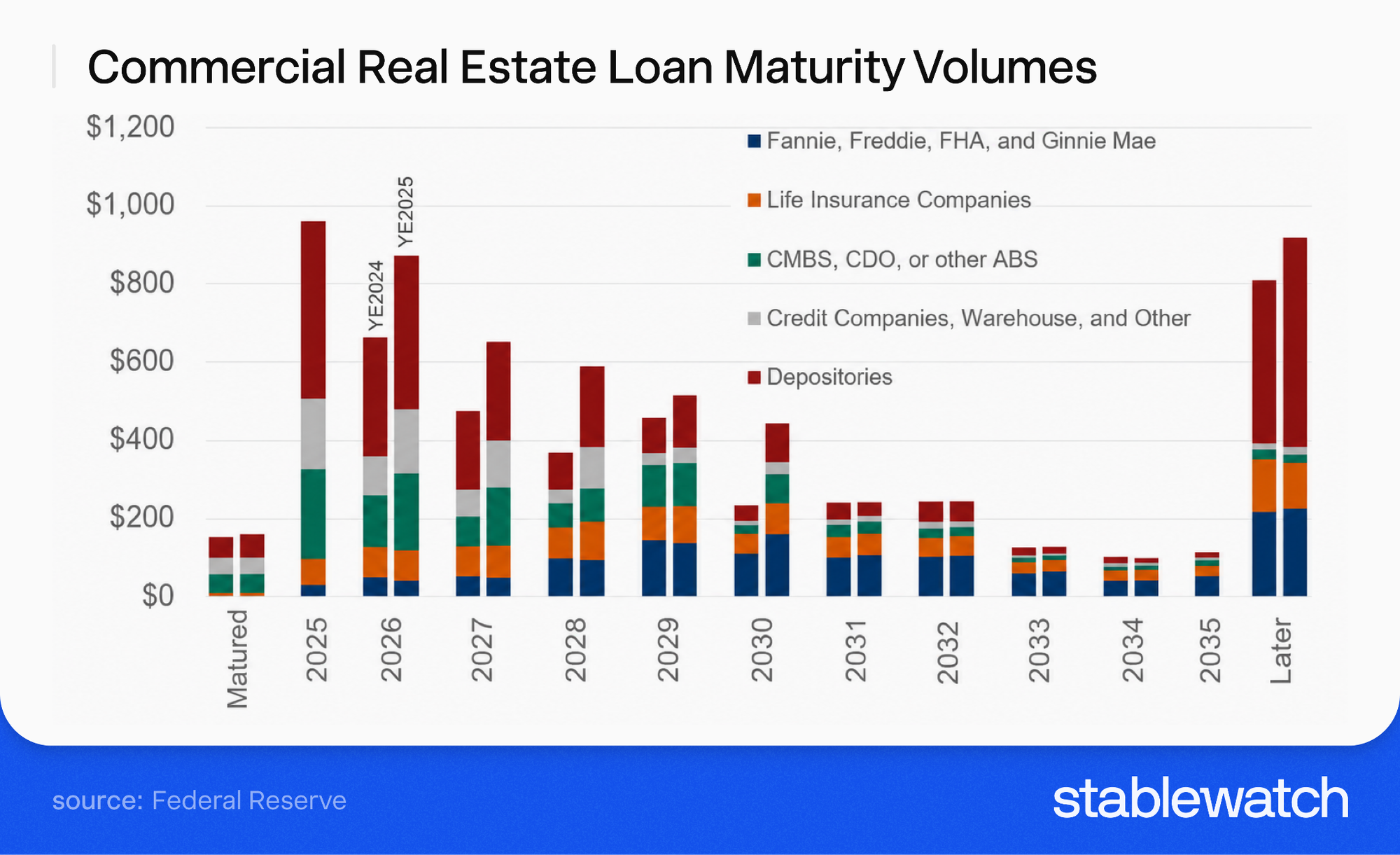

A record $875 billion in US Commercial Real Estate (CRE) debt is scheduled to mature in 2026, and banks hold the largest share: $396 billion, concentrated in the regional and community banks that are least able to absorb it. Mortgage Bankers Association (MBA) data confirms that this maturity wave forces local institutions to protect their own capital instead of paying competitive rates to depositors. Refinancing the maturing debt ties up the cash that could otherwise fund higher deposit yields. The result is that the institutions traditionally closest to retail savers can no longer fight to keep those savers, and the demand for yield migrates to platforms outside the traditional banking system.

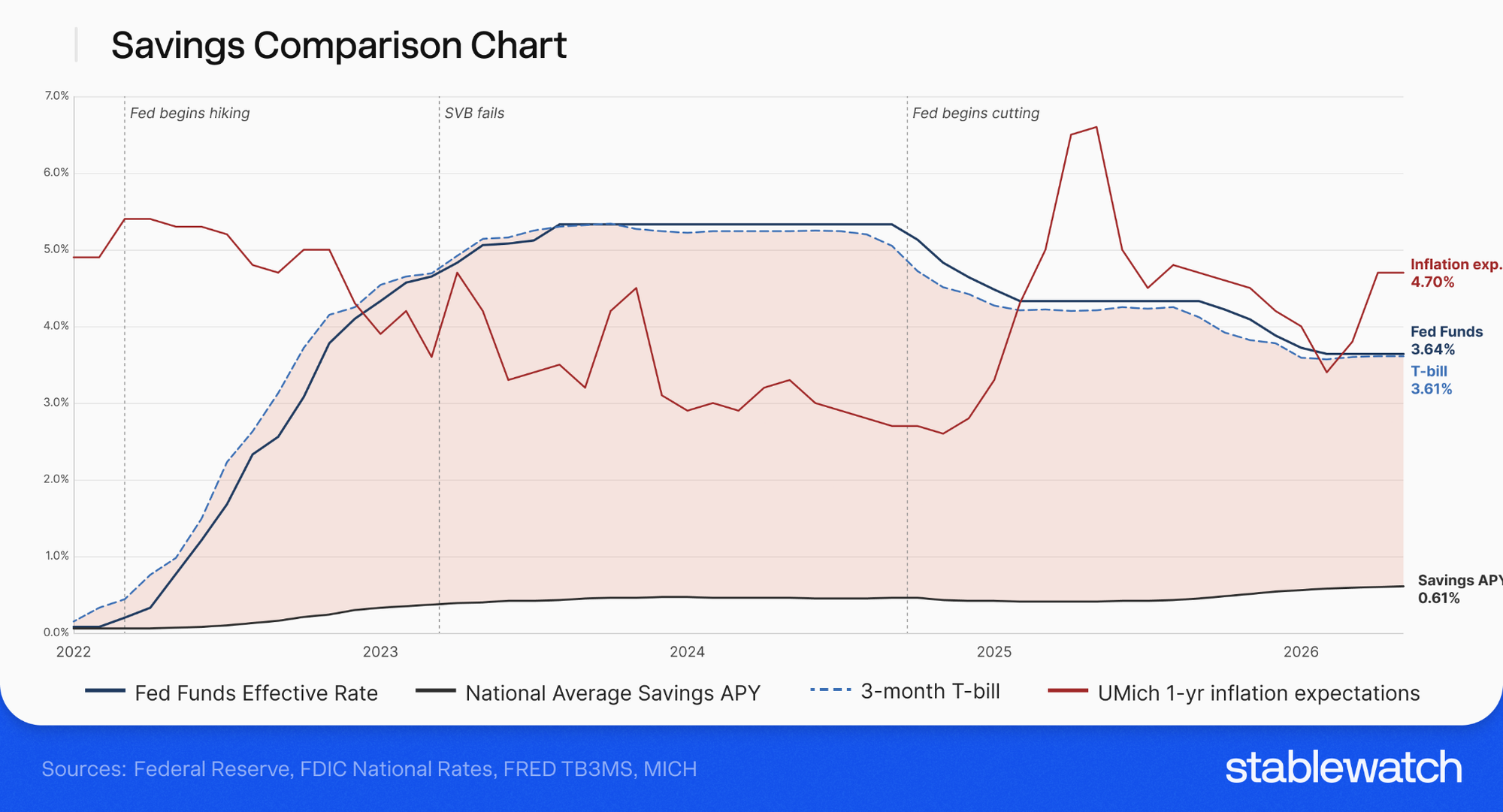

Despite the approaching maturity wave, the banking industry just posted a 3.39% net interest margin (difference between what a bank earns on loans and pays out on deposits), representing the highest reading since 2019. FDIC Quarterly Banking Profile data shows that this margin expanded even as banks originated fewer loans. Banks achieved these record margins by holding deposit rates near zero while loan rates stayed high. Maximizing the spread between earning assets and liability costs remains the primary tool banks use to rebuild capital buffers, and the cost falls directly on retail customers holding cash in traditional accounts.

This divergence suggests that sub-1% savings rates are not just a competitive oversight, but a necessity for banks defending franchise margins while sitting on $306.1 billion in unrealized losses on long-duration Treasuries and Mortgage Backed Securities (MBS) loaded at 1.5-2% yields in 2020-2021. The Fed’s subsequent rate hikes collapsed the market value of those bonds, and Held-To-Maturity (HTM) accounting only defers the hit so long as banks do not sell. Returning capital to depositors would immediately erode the artificial profitability keeping many regional franchises solvent.

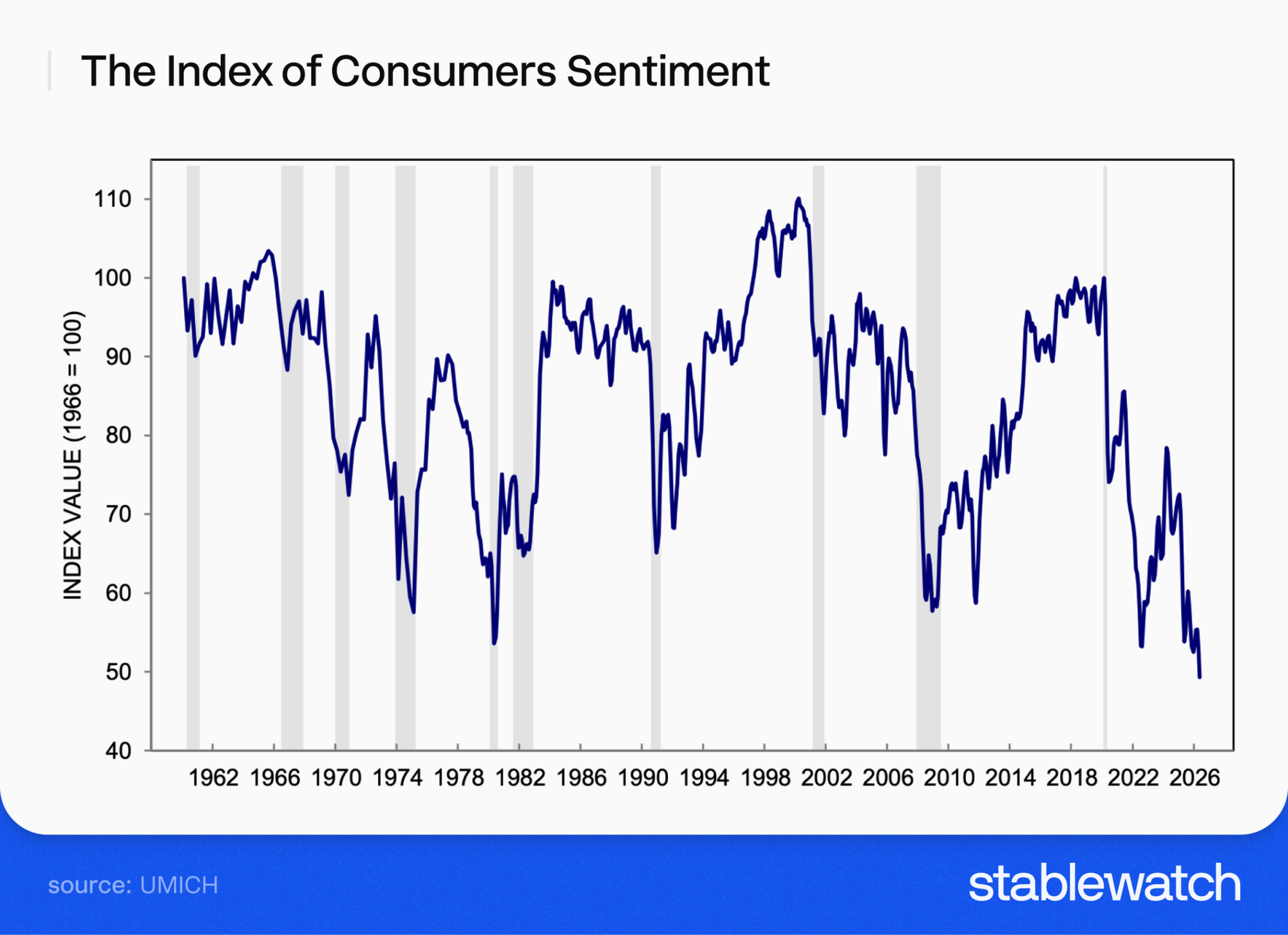

The consumer side of this equation is equally distressed. Bankrate data places the spread between the average credit card APR and the average savings yield at 20.4 percentage points, the widest asymmetric cost of money on record. At the same time, University of Michigan Index of Consumer Sentiment has fallen to 44.8, the lowest reading in 75 years of tracking, while the New York Fed's Q1 2026 Household Debt and Credit Report (released May 12, 2026) places aggregate household debt at $18.8 trillion. UMich's own survey places year-ahead inflation expectations at 4.8% and long-run at 3.9% — figures that turn any sub-1% savings account into a guaranteed real loss.

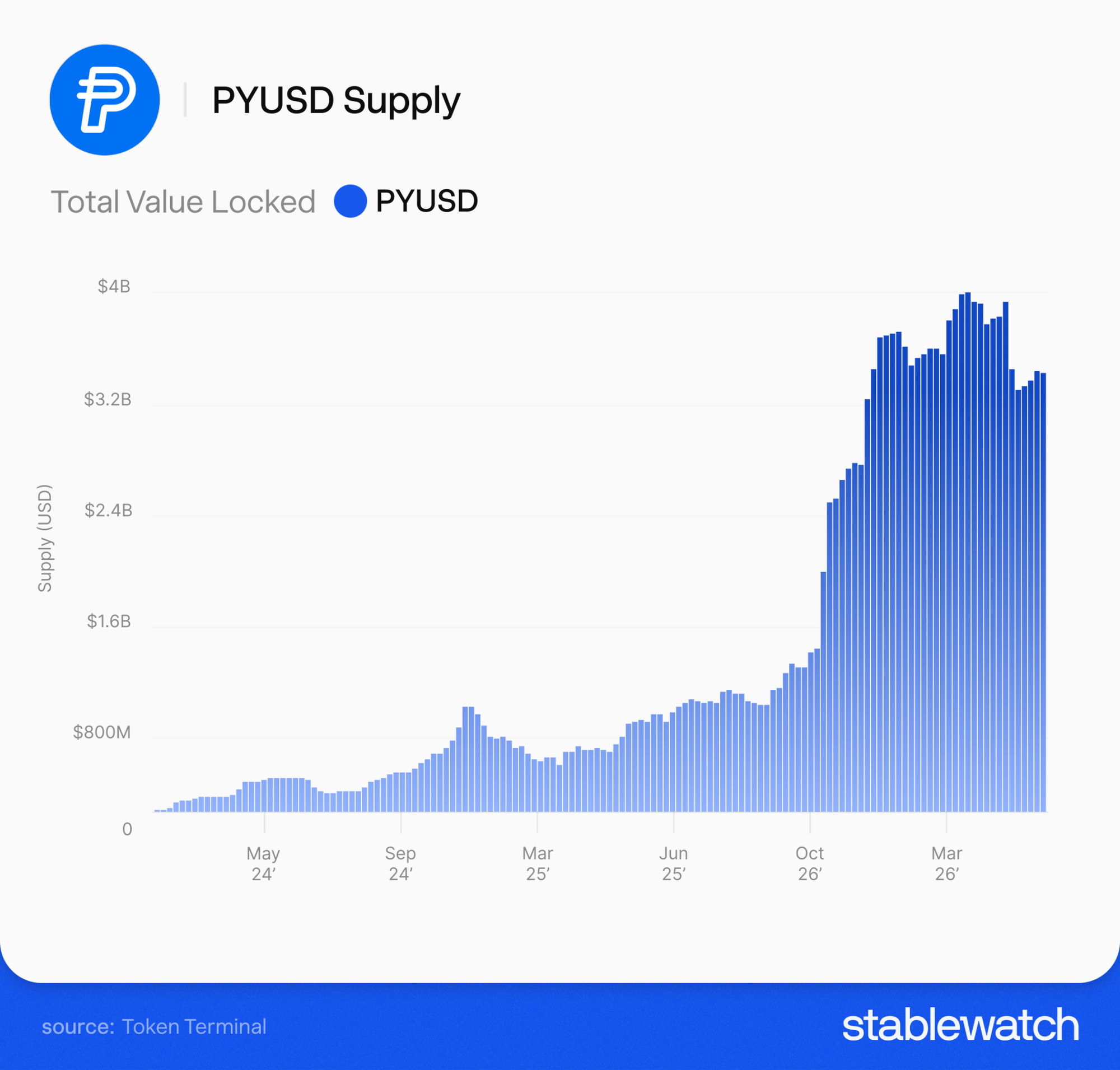

Major financial institutions have already conceded the disruption. In his April 2026 letter to JPMorgan shareholders, Jamie Dimon writes about competitors emerging on blockchain, highlighting stablecoins and tokenization in particular. Robinhood's cash sweep already pays 3.35%, more than five times the 0.61% bank average. PayPal’s PYUSD growing to $4 billion market capitalization.The question is no longer whether the consumer yield rail migrates outside the legacy banking system, but which infrastructure carries the migration.

Osero, a new Sky Prime Agent incubated by Stablewatch, is building that infrastructure. Two distinct products are set to solve the problems discussed throughout this memo: the Osero Earn SDK for fintechs and neobanks integrating the Sky Savings Rate and the Osero App as the direct-to-consumer interface.

The Paralysis of Regional Bank Deposits

$396 Billion Refinancing Wall

Depositories (mainly banks) hold $396 billion of the 2026 commercial and multifamily mortgage maturity wall. MBA data indicates that this concentration of maturing debt creates a serious cash-flow problem for institutions heavily exposed to local real estate. Refinancing this debt forces banks to recognize losses on properties whose values have fallen, while still meeting regulatory compliance. Because of this specific exposure, depositories will remain defensive across upcoming quarters.

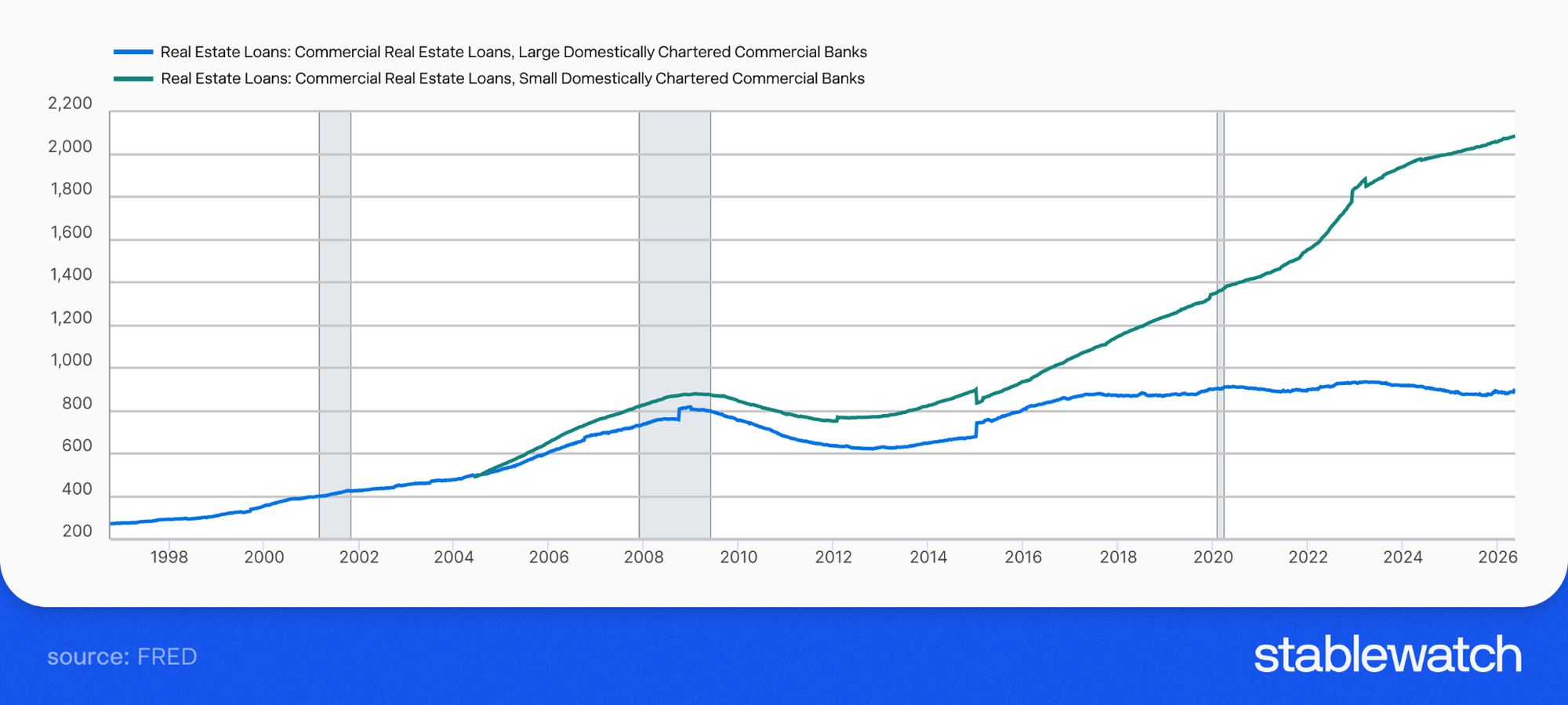

Federal Reserve’s weekly H.8 release on commercial bank balance sheets documents a severe concentration risk, with small banks carrying over $2 trillion in commercial real estate loans compared to $896.5 billion at large institutions. An imbalance of this scale means that the localized community banks traditionally relied upon for competitive savings products are precisely the institutions encumbered by maturing real estate exposure. The risk falls disproportionately on smaller banks, which lack the diversified income streams of the major Wall Street firms. Consequently, these regional players must prioritize survival ahead of paying higher yields.

How Non-Bank Financial Institutions Captured All of 2025's Bank Loan Growth

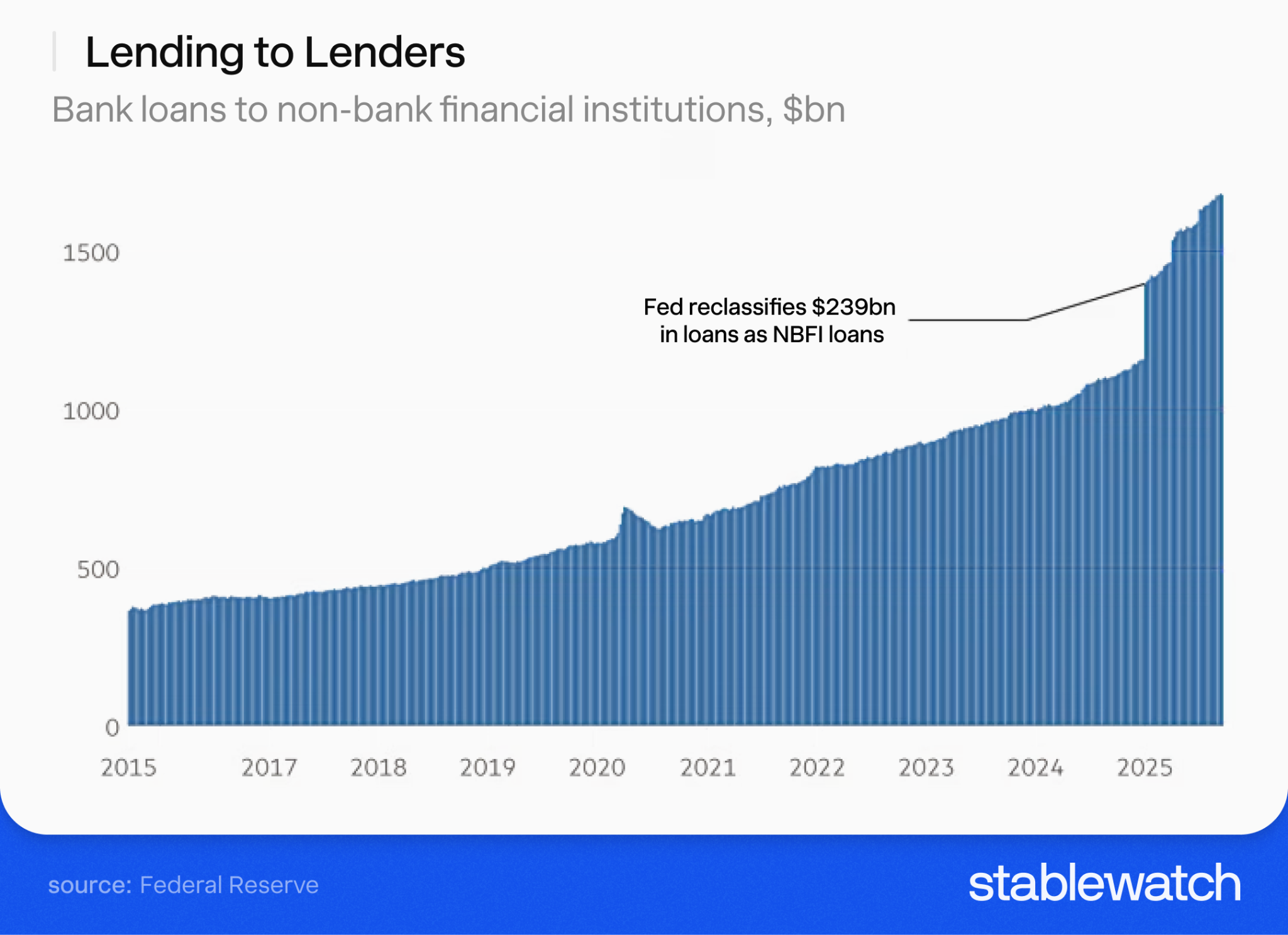

Banks are increasingly routing credit growth through Non-Bank Financial Institutions (NBFIs) rather than expanding direct lending. The New York Fed’s Liberty Street Economics documents that this migration has intertwined regulated banks with a sprawling web of alternative credit providers. Depositors sitting on sub-1% savings accounts are indirectly funding that web, bearing the tail risk through their bank’s solvency while most of the spread captured on those loans stays with the bank.

In 2025, every dollar of net US bank loan growth came from lending to non-bank entities. Direct lending to households and businesses was flat or declining, while wholesale credit to private credit funds, mortgage REITs, and specialty lenders absorbed all new origination. Liberty Street Economics documents this as traditional institutions outsourcing their primary lending function. Relying on shadow banking for growth creates a dependency that ties bank liquidity tightly to the performance of these unregulated intermediaries. Consequently, banks operate more as wholesale funders than direct retail partners.

Liberty Street identifies approximately 50 bank holding companies with non-bank credit exposures exceeding 100% of their Tier 1 equity capital (the highest-quality loss-absorbing layer under Basel III banking regulation), with extreme cases running 4–6× of that capital base. Because of this concentration, a disruption within the private credit or specialty finance markets would immediately threaten the core capital of these institutions. Defending against shadow banking contagion leaves these holding companies without the flexibility to increase retail deposit rates.

Why 300 bps CCC Spread Widening Signals a Higher-For-Longer Regime

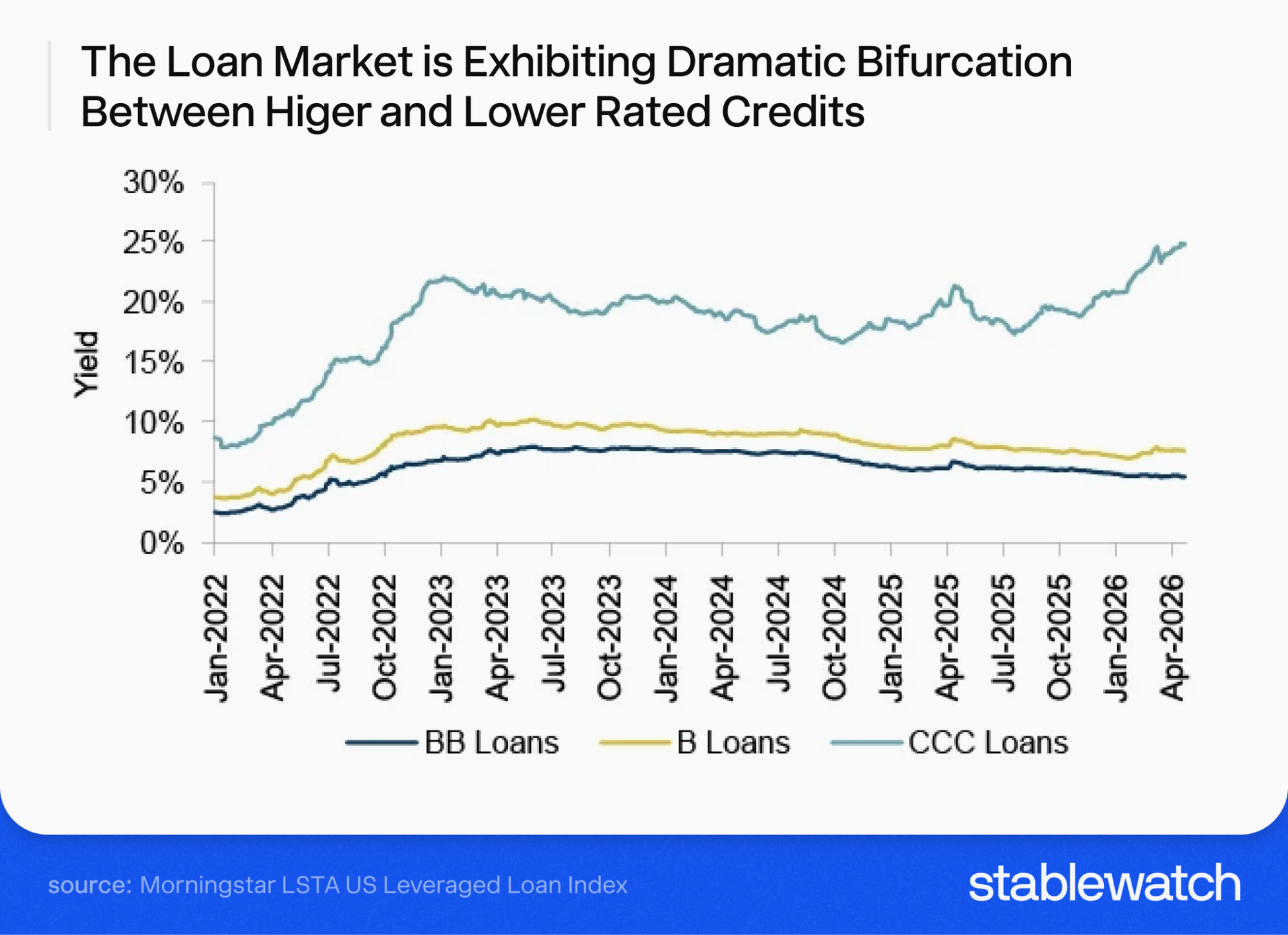

The broader credit market is currently experiencing significant dispersion, with Oaktree Capital noting a 300 basis point widening in spreads on CCC-rated loans (the lowest tier of speculative-grade credit, one step above default). This metric indicates a fracture in how institutional capital assesses varying tiers of corporate risk. Rising defaults among lower-quality borrowers contrast sharply with the stable performance of investment grade credit tranches. Widening spreads suggest that market participants expect sustained economic friction to punish weaker balance sheets.

Against this backdrop, JPMorgan's Jamie Dimon is positioning for a higher-for-longer regime characterized by stickier inflation. In his April 2026 letter to shareholders, Dimon argues that the structural forces of the current cycle will keep borrowing costs elevated for an extended duration. Preparing for this environment requires financial institutions to lock in long-term capital while managing their short-term liabilities. Given this expectation of persistent inflation, consumer deposit rates will remain suppressed as banks protect their net interest margins.

The Office of the Comptroller of the Currency Semiannual Risk Perspective and FDIC quarterly profile both flag these compounding risks as challenging traditional banking oversight models. Official supervisory commentary indicates that the collision of real estate devaluation, shadow banking exposure, and persistent inflation creates a systemic hazard. Supervisors are increasingly concerned that existing capital frameworks fail to capture the true fragility embedded within regional bank portfolios. Pressured by supervisory scrutiny, institutions adopt conservative capital deployment strategies and lose any appetite for retail rate competition.

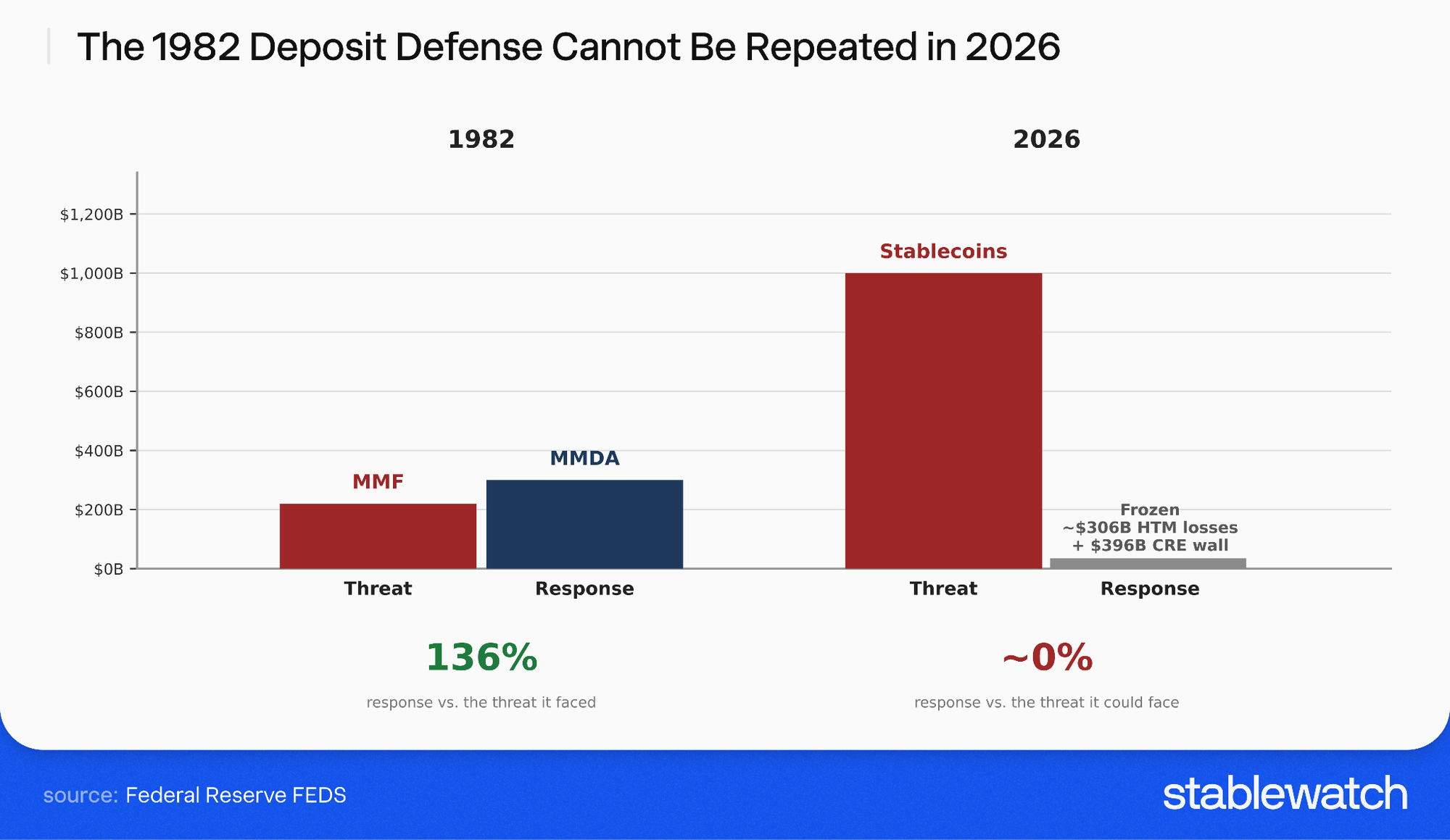

In 1982, Money Market Funds (MMFs) had drained $220 billion out of the banking system (roughly 15% of total bank deposits), before banks successfully deployed Money Market Deposit Accounts (MMDAs) to pull $300 billion into the new accounts within three months. This story and its consequences are discussed in the recent Federal Reserve FEDS Note “Banks in the Age of Stablecoins: Lessons from Their Historical Responses to Financial Innovations” from May 2026. During that era, unencumbered balance sheets allowed traditional depositories to counter the rise of external mutual funds by offering market-rate yields. Successfully executing that defensive maneuver required institutional agility and a relatively clean portfolio of underlying assets. That rapid recapture demonstrates what a healthy banking system can accomplish when threatened by alternative financial rails. The modern analog of that threat is far larger: the FEDS Note “Banks in the Age of Stablecoins: Implications for Deposits, Credit, and Financial Intermediation” from December 2025 projects that up to $1 trillion in deposits (over four times the 1982 MMF threat) could migrate into stablecoins, resulting in a drain of as much as $1.26 trillion from commercial bank lending capacity.

Today, the sheer magnitude of unrealized losses and concentrated commercial real estate debt severely restricts banks from mounting a similar counter-offensive. A 1982-style competitive yield campaign is constrained by the same locked-in HTM and CRE exposures discussed above — mounting such a defense through deposit rates would force regional banks to crystallize the very losses they are working to defer. Defending the existing deposit base through competitive rates is mathematically impossible for banks trapped by these legacy exposures. Emerging financial technology platforms therefore face an uncharacteristically weak defense from incumbent institutions.

How a 20-Point Spread Extracts Wealth From US Households

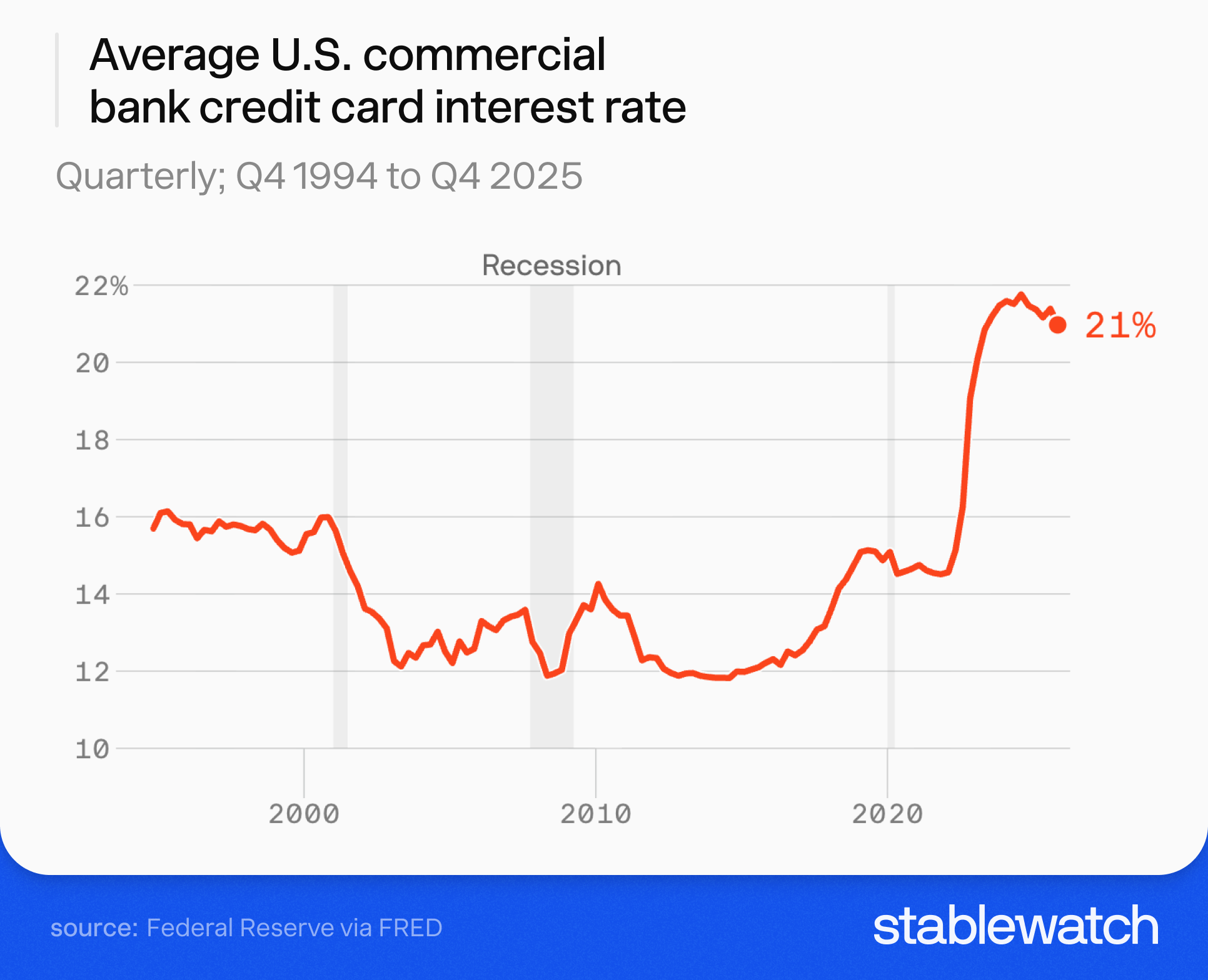

Consumers are currently caught in an unprecedented asymmetry, facing a nearly 20.4 percentage point spread between the cost of borrowing and the yield on deposits. Bankrate's May 2026 reading demonstrates that this chasm represents one of the most extractive margin environments in modern retail banking history. Charging premium rates for credit while paying near-zero returns on savings systematically drains capital from everyday households. The divergence is structurally unstable, and it penalizes the captive retail customer at every step.

The Fed’s G.19 monthly release on consumer credit places the average credit card APR at 21.00% across all accounts, rising to 21.52% for the roughly half of accounts carrying a balance and actually assessed interest — the cohort bearing the squeeze. These elevated carrying costs disproportionately impact middle-class families relying on revolving credit for essential expenses. Sustaining these borrowing rates guarantees continued deterioration of the borrower's financial health.

Conversely, the national average savings account yield lingers at a mere 0.61%, effectively facilitating wealth transfer from households to financial institutions. Earning less than one percent on liquid savings ensures that consumer purchasing power silently evaporates over time. Wealth extraction at this scale relies entirely on the inertia of a captive customer base struggling to access institutional-grade yield products.

Consumer Sentiment Collapses Under $18.8 Trillion in Leverage

This systemic wealth extraction has driven the University of Michigan Index of Consumer Sentiment down to 44.8, its lowest recorded level in 75 years of tracking, and the Surveys of Consumers details a pervasive psychological exhaustion among households ground down by the asymmetric cost of capital. Enduring record-high borrowing costs alongside non-existent savings yields breaks consumer confidence in the financial system. At 44.8, the index reads as a population already willing to search for alternatives to legacy banking relationships.

Compounding the psychological exhaustion, aggregate domestic household debt recently reached a record high of $18.8 trillion. The New York Fed's Q1 2026 Household Debt and Credit Report, released May 12, 2026, documents that this unprecedented leverage requires families to dedicate an increasing percentage of their monthly income to debt service. Managing this massive obligation limits discretionary spending and erodes personal savings buffers further. The sheer scale of the debt ensures that any future macroeconomic shock will translate into severe consumer distress.

Inflation Expectations Turn Low-Yield Savings Into a Real Loss

Persistent inflationary pressures exacerbate the impact of this asymmetric cost of money. UMich Surveys of Consumers place year-ahead inflation expectations at 4.8% with long-run expectations at 3.9%. The New York Fed's Survey of Consumer Expectations corroborates the persistence, placing 1-year inflation expectations at 3.6% and the 5-year horizon at 3.0% — every one of those readings sits well above the 0.61% savings yield. Anticipating consistent currency debasement forces consumers to view traditional banking as an active threat to their stored wealth. Driven by this expectation, the pursuit of alternative yield sources is required just to maintain purchasing power. Households are actively seeking mechanisms to preserve their capital, abandoning traditional depositories as a rational defensive maneuver against inflation. The migration signals a fundamental break in the consumer loyalty that banks relied upon to maintain cheap funding.

Why Major Fintechs Are Already Passing Yield Through to Consumers

JPMorgan CEO Jamie Dimon named this disruption directly in his April 2026 letter to JPMorgan shareholders: "A whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts and other forms of tokenization." Identifying this threat at the highest levels of global finance validates the premise that alternative payment rails represent a challenge to traditional banking. In the same letter, Dimon acknowledges JPMorgan's own response — "building upon our capabilities in global payments and digital assets." Even the ones being disrupted are building on blockchain rails.

Two Defensive Plays from Legacy Fintech

Yield passthrough is already viable at the retail-broker layer. Robinhood’s Gold cash sweep pays 3.35% and the non-Gold sweep around 1.5%, both well above the 0.61% bank average. The mechanism is straightforward: customer cash sits at FDIC-insured partner banks earning Treasury-bill yields, and Robinhood returns most of that yield to users while keeping a spread. The model is the inverse of the bank approach: capture some of the spread, distribute the rest. Any platform that doesn’t move toward yield-bearing cash will bleed balances to crypto-native alternatives that already do.

PayPal's PYUSD stablecoin recently achieved a $4 billion market capitalization. The scale of a Web2 issuer at this level validates stablecoin infrastructure as a mandatory layer of modern fintech, but it also exposes the limits of traditional stablecoin deployment. PayPal captures the T-bill yield on the reserves backing PYUSD, while users holding it in the PayPal app earn nothing on those balances unless they route their tokens off-platform into DeFi venues. The gap between the yield that the issuer earns and the yield received by the user is the integration opportunity: fintech platforms need yield-distribution rails that pass the spread through natively, without forcing users to bridge into protocols they don’t understand.

Network Effects vs. the Cold Start Problem

Despite the commoditization of base-layer infrastructure, established consumer distribution channels remain difficult for new entrants to replicate. Convincing a user to abandon a deeply integrated legacy banking app requires more than a slightly improved interface — it needs a financial incentive that helps break established habits. Offering stablecoin yields well above the 0.61% bank average provides exactly that incentive, turning the suppressed deposit rates into a customer-acquisition tool for any platform that can deliver the alternative. The strategic question for emerging crypto neobanks reduces to whether the platform can source, secure, and pass through that yield reliably enough to support sustained acquisition.

When Yield Becomes Table Stakes

As attractive yield offerings transition from a competitive advantage to a baseline market expectation, the battlefield shifts toward the architecture of yield distribution. Simply offering a high rate is no longer sufficient; the platform must reliably source, secure, and deliver that yield without exposing the user to systemic risk. Mastering this backend architecture allows platforms to scale without the capital constraints that throttle traditional banks. The transition demands a re-engineering of how fintech companies manage treasury operations and counterparty exposure.

Success in this new paradigm requires abstracting the underlying complexity of blockchain mechanics into a seamless, intuitive consumer interface. The winning applications have to present users with a familiar, Web2-style banking experience while silently running decentralized rails on the backend. A well-built abstraction layer is what bridges institutional-grade onchain yield with mass-market consumer adoption.

The capitulation of major legacy incumbents discussed above, indicates that the strategic pivot toward a yield-centric model is an irreversible necessity for the broader financial technology sector. Adapting this change requires existing platforms to dismantle their historical revenue engines and embrace volume-based economics. Forced evolution accelerates the deployment of decentralized financial infrastructure across consumer touchpoints.

Osero Earn: The Stablecoin Savings Infrastructure

While the strategic necessity of passing yield to consumers is clear, almost no platform possesses the in-house capability to build the institutional-grade yield-generating stack from scratch. The work spans treasury, custody, smart-contract risk, liquidity management — requiring substantial capital outlay, specialized technical talent, and an operational team large enough to monitor every layer continuously. Small fintech teams attempting it in-house frequently produce structural failures, and the engineering cost diverts resources away from the user-acquisition work where these platforms actually compete. The cold-start problem is therefore an infrastructure problem: emerging payment platforms need reliable yield distribution without taking on the prohibitive burdens of direct asset management — and the market opening is for plug-and-play infrastructure built specifically for that purpose.

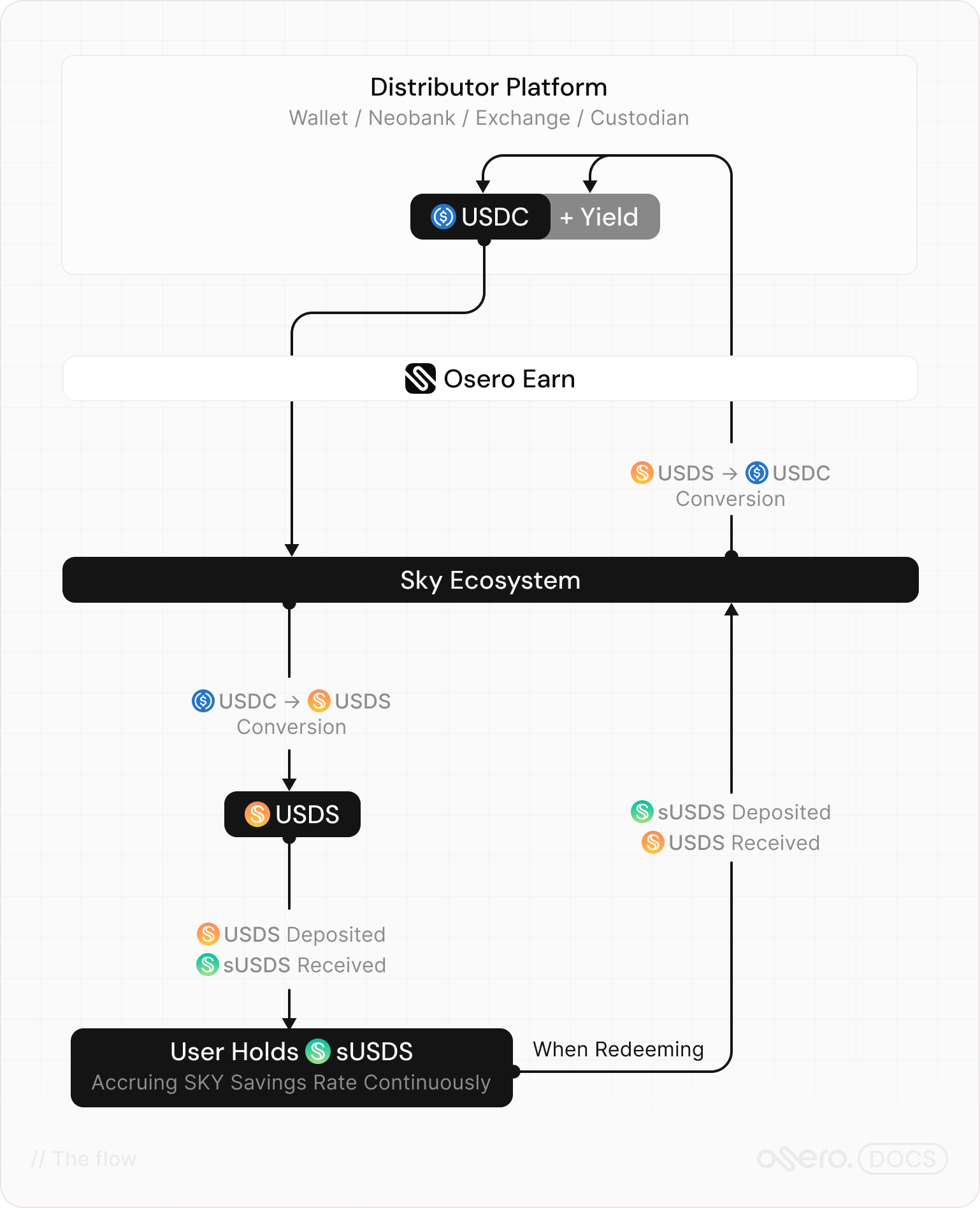

Osero Earn addresses this gap, operating as a dedicated yield-distribution infrastructure layer built specifically for wallets, fintechs and neobanks. It sources yield from the Sky Savings Rate, currently (as of June 2026) 3.6% APY against $6.1 billion of sUSDS supply. Specialized risk management and smart contract interaction within a dedicated infrastructure provider significantly reduces the attack surface for the integrating platforms. This positioning allows Osero to capture aggregate volume by serving as the backend engine for numerous consumer-facing applications, connecting them to the leading yield engine.

Packaging Sky Protocol Mechanics Into Osero

The Osero Earn SDK collapses the complexity of DeFi integration and risk methodology into ten lines of code, enabling platforms like wallets, neobanks and exchanges to offer the Sky Savings Rate directly to their users. The SDK currently supports five chains: Ethereum Mainnet, OP Mainnet, Unichain, Base, and Arbitrum One (Plasma coming soon) and abstracts chain-specific routing, Peg Stability Module (PSM) execution, ERC-20 approvals, and ERC-4626 vault deposit logic behind a single client object. Reducing the technical friction accelerates the mass deployment of tokenized yield across diverse consumer applications.

Beyond building yield infrastructure in-house, integrating platforms have the option to contract vault curators to manage the underlying strategy on their behalf. The model does not scale because of liquidity limitations. It also introduces a structural misalignment that compounds under stress: the curator's fee is fixed regardless of outcomes, meaning they bear no financial consequence if the strategy they recommend produces a loss. Sky ecosystem resolves this directly — $175M of risk capital on its balance sheet sits ahead of every user deposit in the loss waterfall, creating explicit financial consequences for infrastructure failures that no curator arrangement can replicate. Platforms that contract curators are outsourcing risk without transferring it.

Why Osero Builds on Sky

Osero’s offer to a fintech or neobank is anchored in Sky’s underlying infrastructure. The Sky Savings Rate provides integrators with a non-volatile APY (3.6% as of the time of this publication) that can be clearly communicated to the retail users. This offer can be contrasted directly with floating-rate lending venues, where yields can sometimes move several hundred basis points within a single week, forcing platforms to continuously update the rates they advertise to users and the treasury returns they forecast internally.

The yield asset, sUSDS, is also the largest in its category, currently sitting at $6.1 billion of supply within $11.2 billion of total USDS, with the deepest onchain liquidity of any yield-bearing stablecoin. This liquidity depth defines how cleanly retail users can enter and exit the position without incurring slippage, and how rapidly B2B partners can rebalance treasury positions during periods of elevated flow. The entire collateral basket, spanning RWA treasury exposure and crypto-native collateral, is fully transparent onchain and auditable in real time.

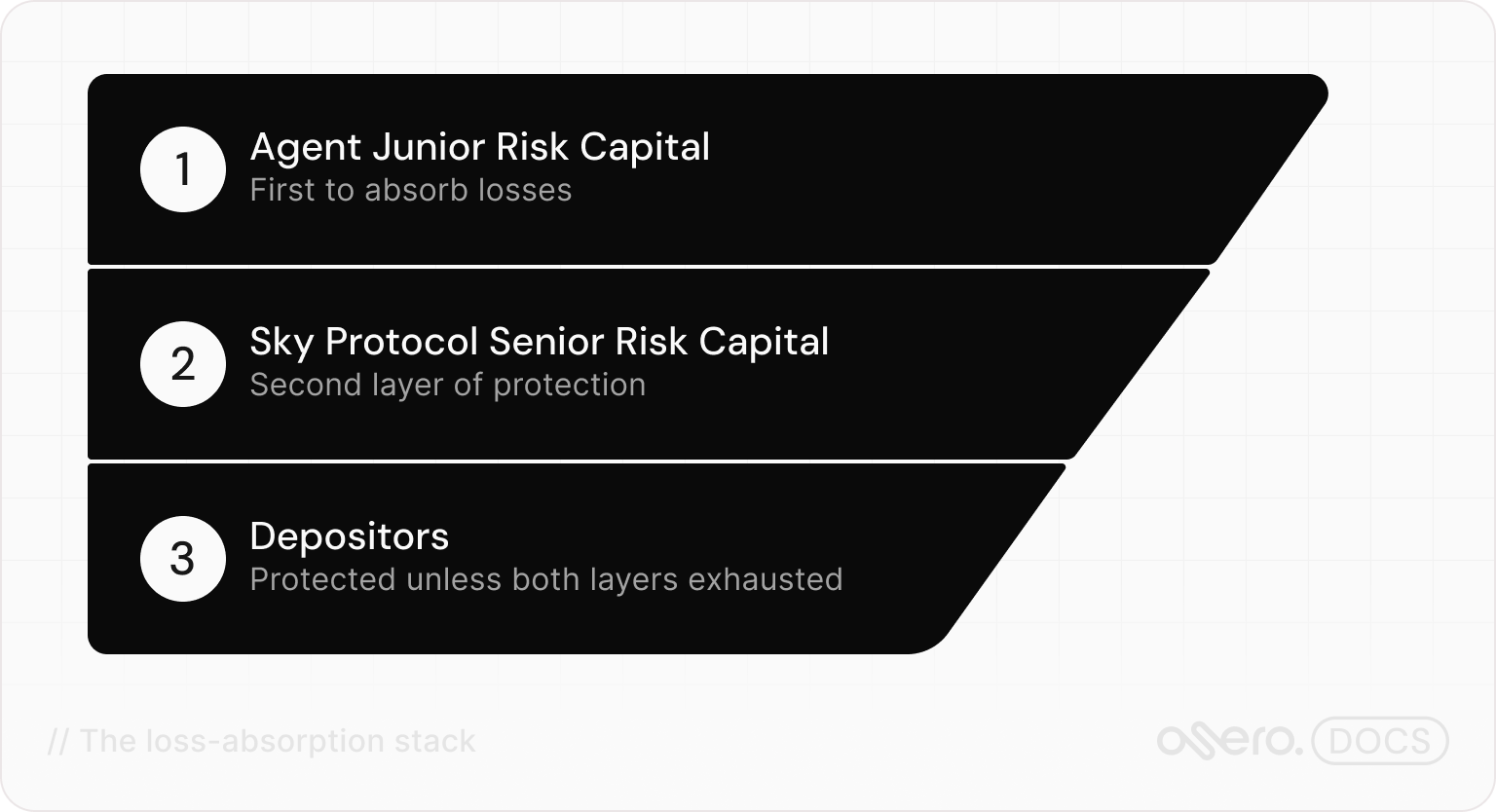

A share of neobank-adjacent crypto yield products today route user funds into isolated lending markets managed by curators whose risk methodology is opaque, or into floating-rate venues where there is no meaningful loss-absorption stack. Recent dislocations in those markets could be understood as consequences of architectures in which users cannot identify whose capital absorbs losses ahead of theirs. Sky’s structure applies a very transparent scheme: junior risk capital takes the first loss, senior risk capital absorbs the second tranche, and depositors remain whole unless both prior layers are fully exhausted. Osero’s users can map their position in the loss waterfall by referencing a single page of documentation.

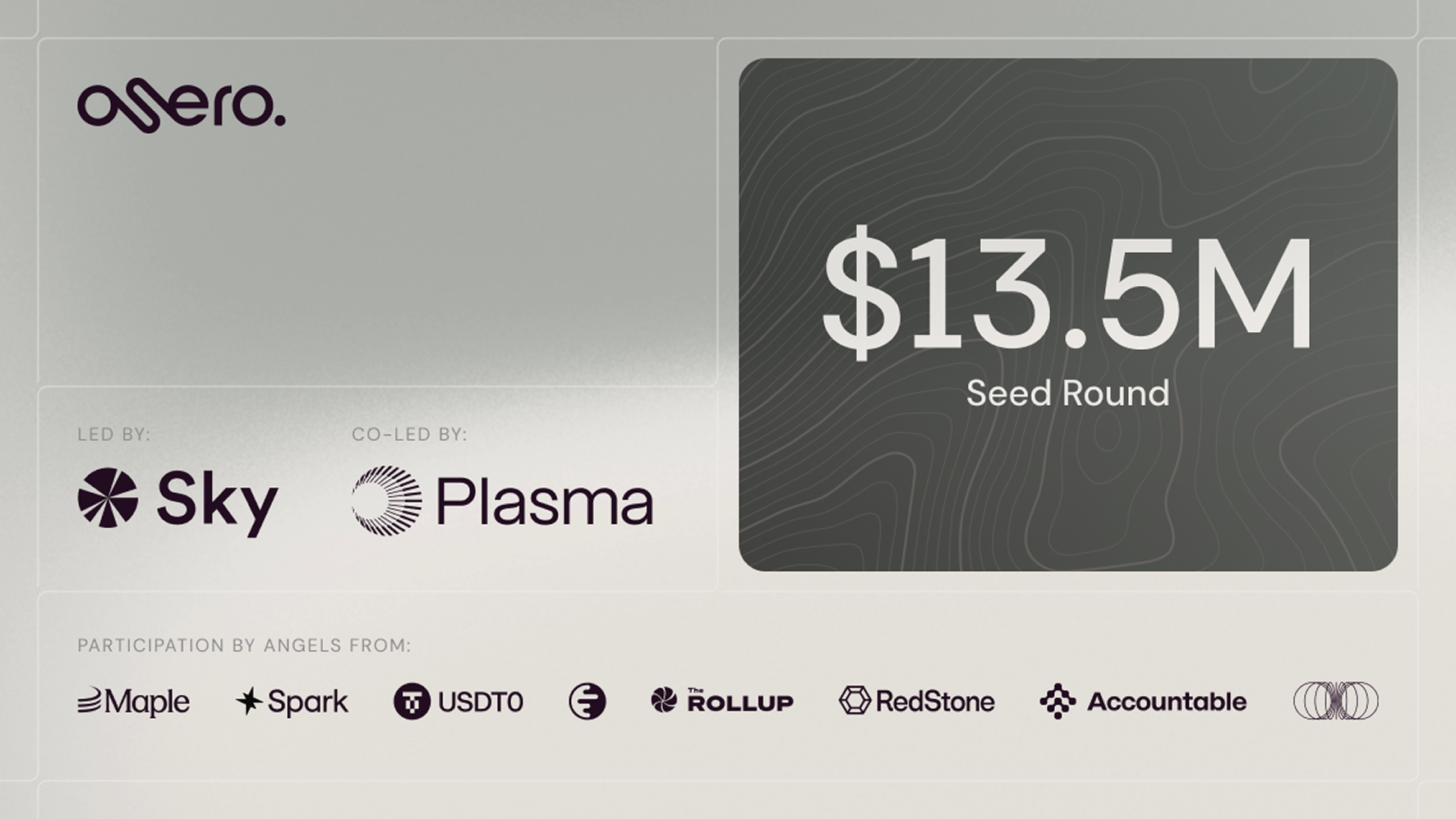

This is the architecture Osero is built on. The recent $13.5 million seed round led by the Sky Ecosystem and co-led by Plasma was structured to fit Sky’s loss-absorption hierarchy. $10 million of that funding becomes junior risk capital on Osero’s balance sheet, protecting Sky’s senior capital and taking first-loss exposure. Across Sky’s broader agent network, junior risk capital aggregates to $111 million; Osero contributes a meaningful share. The signal to a fintech partner is clear: the infrastructure provider holds first-loss exposure alongside the protocol it distributes.

By inheriting proven risk-tranching methodologies from traditional financial institutions, this Basel III-inspired capital stack provides a familiar framework for institutional due diligence teams. Connecting decentralized yield generation with TradFi-grade capital structuring creates a backend solution for the next generation of neobanks. The result is the financial durability required to process aggregate stablecoin volume at scale.

$1 Trillion Deposit Migration

The three threads of this memo: paralyzed regional banks, exhausted consumers, and maturing yield-distribution infrastructure; now meet a scale test. As legacy banks remain frozen by unrealized losses, consumers will route capital through specialized fintech platforms to escape punitive inflation. The deployment of institutional-grade SDKs like Osero effectively removes the final technical barrier preventing the capital migration. The convergence of distress and innovation is poised to catalyze permanent reallocation of retail liquidity.

Federal Reserve analysis projects that a $1 trillion migration of liquidity into stablecoins could trigger an outsized contraction of up to $1.26 trillion in overall commercial bank lending capacity. The model demonstrates that draining low-cost deposit funding directly forces regional banks to curtail their origination of local business and real estate loans. Starving these institutions of cheap retail capital permanently impairs their ability to function as the primary credit engine for the American economy. A contraction of that magnitude would compound directly with the deposit suppression.

The longer term consequence sits one layer deeper. Specialized lenders: commercial real estate originators, small-business credit funds, equipment finance providers; built their business model around accessing low-cost deposit funding through regional bank relationships. As that funding base contracts under deposit migration, those lenders will be forced to seek capital where retail liquidity has now accumulated. Sky’s architecture is purpose-built to absorb that reallocation. Specialized lenders plug into the network as Halo Agents drawing capital from Prime Agent allocators like Osero, which in turn source from the stablecoin liquidity. The credit-creation function migrates with them, restructured around stablecoin flows and intermediated by an agent network that prices risk explicitly.

And unlike the rapid recapture of deposits achieved with money market accounts in 1982, legacy banks today remain throttled by real estate and shadow banking encumbrances. Paralyzed by underwater assets and regulatory scrutiny, traditional banks can only watch as the consumer yield rail migrates outside the legacy perimeter. The infrastructure carrying that migration is yield-distribution architecture purpose-built for the integrator layer and Osero is building that infrastructure, directly aligned with the Sky network's upstream yield. The migration is no longer a question of whether, but of how fast.

SOURCES:

- https://www.oaktreecapital.com/insights/insight-commentary/market-commentary/dispersion-revisited

- https://www.jpmorganchase.com/ir/annual-report/2025/ar-ceo-letters

- https://www.fdic.gov/news/speeches/2026/fdic-quarterly-banking-profile-fourth-quarter-2025

- https://www.occ.treas.gov/news-issuances/news-releases/2026/nr-occ-2026-35.html

- https://libertystreeteconomics.newyorkfed.org/2026/05/stress-and-strain-from-nbfis-to-banks/

- https://newslink.mba.org/mba-newslinks/2026/february/mba-newslink-tuesday-feb-10-2026/17-of-commercial-and-multifamily-mortgage-balances-to-mature-in-2026/

- https://www.bankrate.com/banking/savings/average-savings-interest-rates/

- https://www.sca.isr.umich.edu/

- https://www.newyorkfed.org/newsevents/news/research/2026/20260512

- https://www.newyorkfed.org/newsevents/news/research/2026/20260507

- https://www.federalreserve.gov/releases/h8/current/

- https://www.federalreserve.gov/releases/g19/current/

- https://www.federalreserve.gov/econres/notes/feds-notes/banks-in-the-age-of-stablecoins-lessons-from-their-historical-responses-to-financial-innovations-20260501.html

- https://www.federalreserve.gov/econres/notes/feds-notes/banks-in-the-age-of-stablecoins-implications-for-deposits-credit-and-financial-intermediation-20251217.html

- https://robinhood.com/us/en/support/articles/cash-sweep-program-interest-rate/

- https://thedefiant.io/news/tradfi-and-fintech/paypal-pyusd-supply-crosses-usd4-billion

- https://www.theblock.co/post/400948/sky-ecosystem-stablewatch-stablecoin-yield-startup-osero-funding

- https://www.stablewatch.io/research/stablewatch-incubates-osero-with-a-13-5m-raise

- https://docs.osero.org/