The Rise of Yield Stablecoins

Yield-bearing stablecoins are on the rise.

You can see this in different metrics tracked on our site: the total market capitalization of yield stablecoins, the number of such products launching over the past months, and the total yield paid out to users.

Let’s dive into the data.

Yield stablecoins are quickly emerging as digital alternatives to traditional money market funds and bank deposits. By offering a stable value and generating passive income, these assets are attracting both institutional and retail users seeking efficient ways to earn yield. Their use in global payments is expanding, enabling seamless international transfers and supporting both decentralized finance (DeFi) and traditional finance systems. DeFi, powered by smart contracts, is the ecosystem that enables these innovations—providing transparent, permissionless, and autonomous infrastructure for yield generation and risk management.

What are yield stablecoins anyway? These are stablecoins that not only maintain price stability but also generate passive income for holders by distributing protocol revenue, staking rewards, or yield from underlying assets. Yield stablecoins aim to maximize capital efficiency, allowing users to earn returns on their assets without sacrificing liquidity or security.

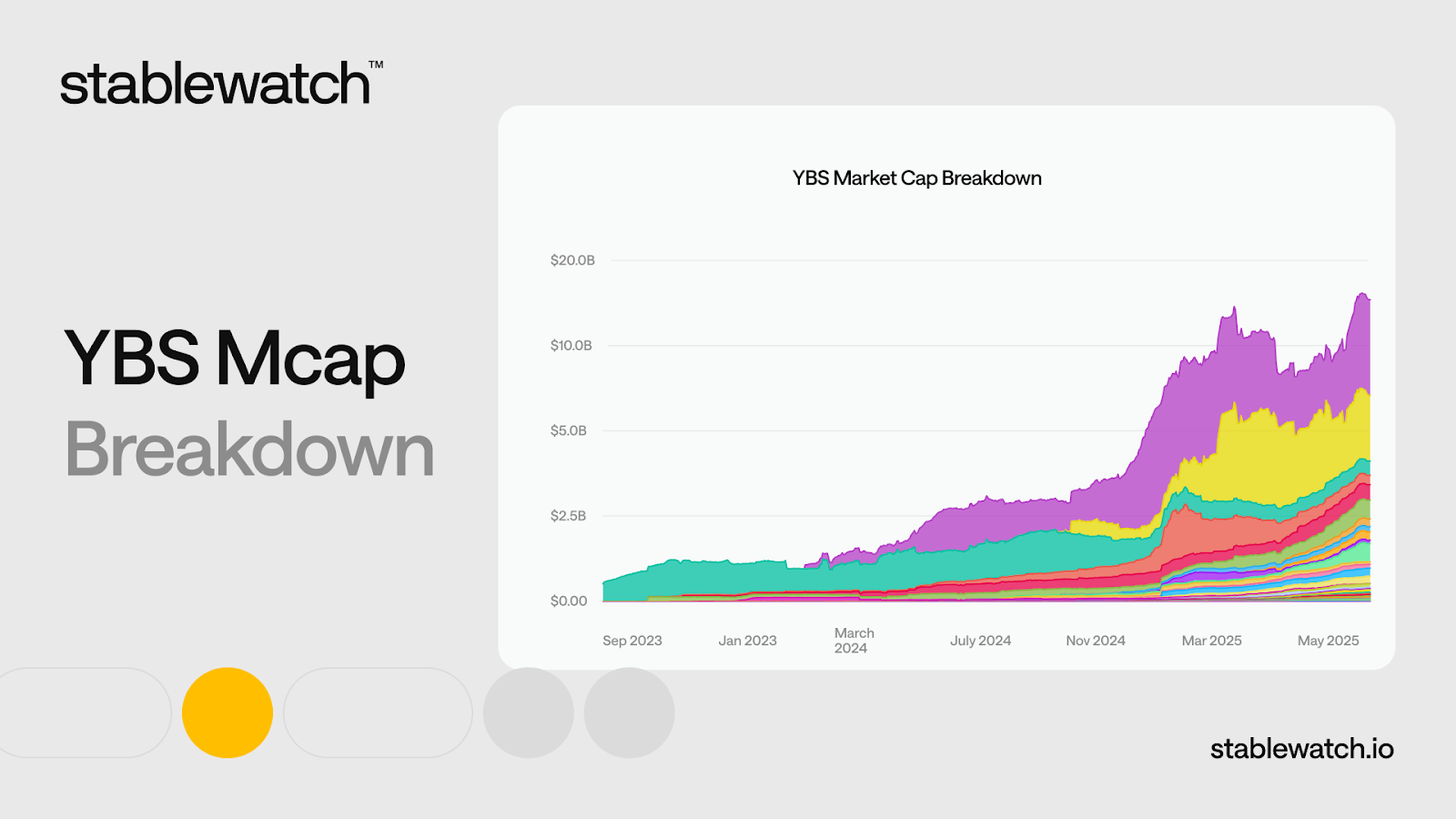

Market cap of yield bearing stablecoins

Over less than two years, their total supply has increased 13x, reaching $11.06 billion in Mid June 2025, up from just $666 million in August 2023. It reached an all-time high of $11.3 billion in June and has remained steady ever since. The total value and total value locked (TVL) in yield stablecoin protocols are key metrics used to assess the liquidity, market size, and security of these assets, providing insight into the overall health and adoption of the sector:

Compared to payment-first stablecoins (read more about the distinction here: The two types of stablecoins that matter: payments vs yieldurl to our other article ), yield-first stablecoins are still just a small fraction (4.42%) of the general stablecoin market (as of now, $11.96b compared to the total market cap of $250.42b). Stablecoin transaction volumes continue to grow, reflecting the increasing adoption of yield stablecoins in digital payments, DeFi, and cross-border payments:

How many yield stablecoins are out there?

Currently, we track more than 45 yield-bearing stablecoins, but there are more than 100 on our list, and adding the new ones keeps us busy. Note that there is no widely accepted definition of a yield stablecoin, so it depends on how you count (see more below). Here is a chart that shows their respective market capitalization. Liquidity pools, liquidity providers, and decentralized exchanges play a crucial role in enabling yield generation, trading volume, and efficient market access for these assets:

It’s clear that the number is growing rapidly, and many have recently launched and are getting traction now. Look at the same chart, but with the top 6 (as measured by the current market cap) yield stablecoins excluded, and the timeframe zoomed in to the last 12 months:

Not surprisingly, yield stablecoins issued by Ethena (sUSDe) and the first mover in the space, Sky (sUSDS and sDAI), dominate the market with the mentioned assets constituting 58% ($6.42b) of the total market cap of yield stablecoins:

Yield Paid Out (YPO)

Since mid-2023, yield stablecoins have distributed almost $626 million in yield:

Note that the YPO metric, pioneered by us, is still in its infancy and does not track the multiple interdependencies of yield stablecoins. That said, it provides a valuable snapshot overview of the relevance of yield stablecoins as an asset type.

Yield mechanisms for stablecoins include lending platforms, yield farming, liquidity mining, and staking rewards. Protocol revenue from these activities, along with token rewards and multiple yield sources, contribute to the net yield received by token holders. These mechanisms allow users to earn yield and benefit from income generated by various DeFi strategies, with net yields reflecting the actual returns after accounting for costs and risks.

What are yield stablecoins anyway?

There is no widely accepted definition of yield stablecoin. As I mentioned in my previous article linked to before, it’s an extremely broad and diverse category of tokenized yield strategies, hedge fund-like structures, simple asset (e.g., Treasury bills) wrappers, interest-bearing lending receipts, multi-strategy yield aggregators, and so on. Yield-bearing stablecoins differ from non yield bearing stablecoins and traditional stablecoins, which are typically backed by liquid reserves and do not pay interest to holders. Yield stablecoins often use underlying assets and real world assets, such as government bonds or Treasuries, as collateral to generate yield.

One could classify them, among others, by:

- Source of yield,

- Yield distribution mechanism,

- Peg maintenance mechanism,

- Backing type,

- Custody arrangements,

- Regulatory status,

- Liquidity profile and redemption access and cadence,

- Governance model,

- Risk concentration,

- Target user segment

- Infrastructure (chain) availability, etc.

Risks and considerations include liquidity risk, market stress, market volatility, liquidity shortages, and counterparty exposure, making regulatory compliance an important factor for institutional and retail participants.

Some models, such as delta neutral synthetic dollar stablecoins, use hedging strategies and onchain derivatives to maintain their peg and generate yield. Digital assets, including yield bearing tokens, are used in these strategies to produce income and passive yield for token holders.

Much more work and research is needed to shed more light on this emerging phenomenon. Even if yield stablecoins unbundle into multiple other, clearer categories, looking into the economics, technology, and applicable rules will help their users make better decisions and protect market integrity.

This content is for informational purposes only and does not constitute investment advice.